Ultimate Singapore CPF 2026 Guide: Rates, OW Ceiling & Allocation Rules

The Central Provident Fund (CPF) is the cornerstone of Singapore's social security and retirement savings framework. Every working Singapore Citizen and Permanent Resident contributes a portion of their monthly income to CPF, matched by an employer contribution. As we enter 2026, major regulatory adjustments — including the final phase of the Ordinary Wage (OW) ceiling increase — directly impact monthly take-home pay and retirement allocations.

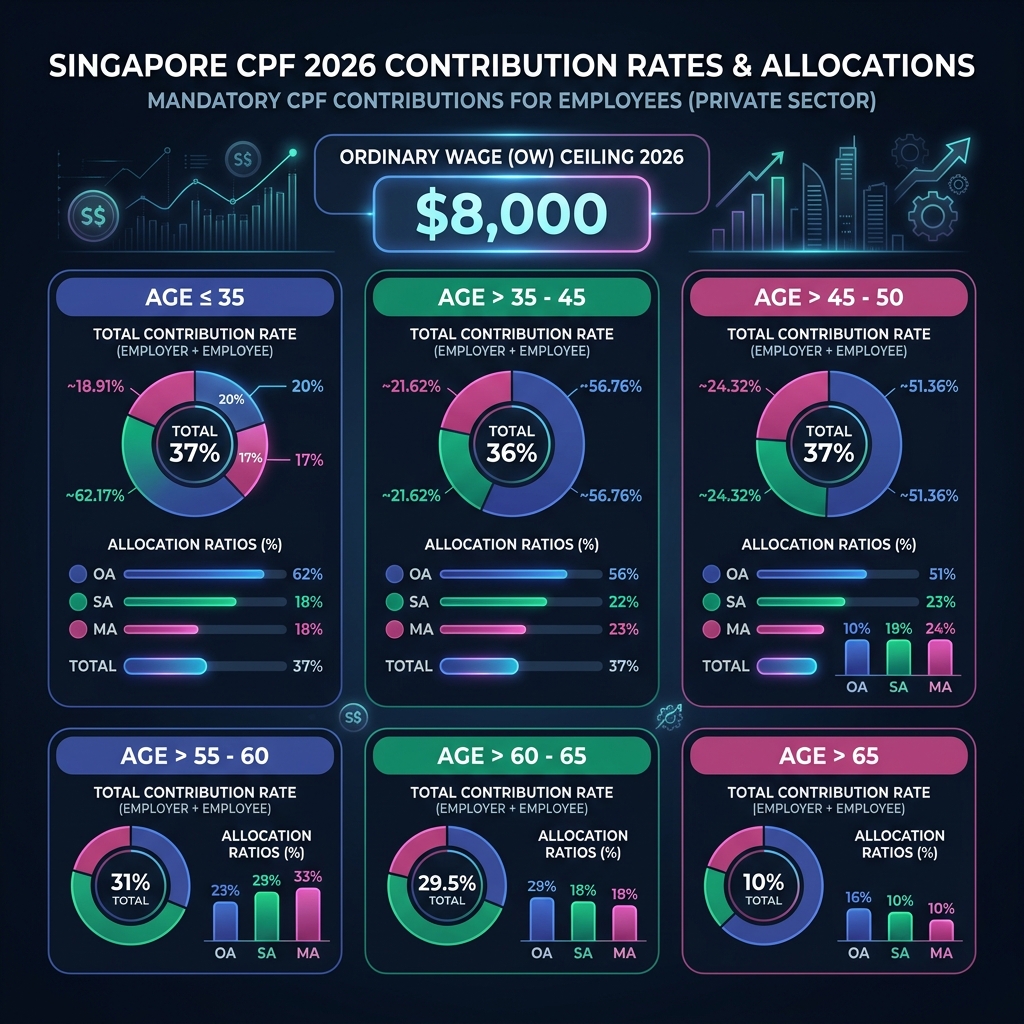

The S$8,000 Ordinary Wage (OW) Ceiling Increase in 2026

To keep pace with rising salaries, the Singapore government progressively raised the monthly Ordinary Wage (OW) ceiling from S$6,000 to S$8,000. Effective 1 January 2026, the ceiling reaches its final targeted cap of S$8,000 per month. This means CPF contributions are calculated on gross wages up to S$8,000; any earnings above this threshold are exempt from statutory CPF contributions.

Figure 1: Visual breakdown of CPF Ordinary Wage ceiling cap and age-dependent allocation splits.

CPF Contribution Rates by Age Group (2026)

For Singapore Citizens and 3rd year+ Permanent Residents, the total CPF contribution rate is 37% of wages for employees aged 55 and below. However, as workers age, contribution rates step down to balance retirement security with employability:

- Age 55 & Below: Employee contributes 20%, Employer contributes 17% (Total: 37%)

- Age 56 to 60: Employee contributes 16%, Employer contributes 18% (Total: 34%)

- Age 61 to 65: Employee contributes 12.5%, Employer contributes 12.5% (Total: 25%)

- Age 66 to 70: Employee contributes 7.5%, Employer contributes 9% (Total: 16.5%)

- Age 71 & Above: Employee contributes 5%, Employer contributes 7.5% (Total: 12.5%)

Where Does the Money Go? OA, SA/RA, and MA allocations

Your total monthly CPF contributions are allocated across three separate interest-bearing accounts. The allocation ratio is dynamic and shifts as you age, prioritizing housing in your early career and transitioning to retirement and healthcare in later years:

- Ordinary Account (OA): Primarily used for housing downpayments, home loan installments, and approved education or investment. Earns a baseline interest rate of 2.5% per annum.

- Special Account (SA): Dedicated to retirement savings, earning a higher interest rate of 4% per annum. Note: At age 55, the Special Account is closed and funds are transferred to the Retirement Account (RA).

- MediSave Account (MA): Reserved for medical expenses, health insurance (e.g. MediShield Life), and approved outpatient treatments. Earns 4% per annum.

Strategic Tips to Maximize Your CPF Growth

- OA-to-SA Transfer: If you do not plan to buy property soon, you can transfer funds from OA to SA to boost your interest rate from 2.5% to 4%. This is a one-way transfer that cannot be reversed.

- Retirement Sum Topping-Up (RSTU) Scheme: Top up your Special Account (if under 55) or Retirement Account (if 55+) with cash. You can get tax relief of up to S$8,000 per year for personal top-ups, and another S$8,000 for topping up loved ones' accounts.

- CPF Investment Scheme (CPFIS): If you are a confident investor, you can invest OA funds exceeding S$20,000 and SA funds exceeding S$40,000 in approved shares, gold, and mutual funds.

Want to see exactly how your salary is split between take-home pay and your CPF accounts? Scroll down to the interactive Singapore CPF Calculator below to key in your salary and age, and see a full monthly and annual breakdown instantly!

Interactive Inline Calculator

Adjust target values below to run formulas in real-time instantly.

Adjust Inputs

Singapore Localized Tool

This calculator is calibrated specifically for Singapore statutory rules, tax brackets, and CPF allocation policies (2026 guidelines).

Calculated Results

CPF Account Allocation Breakdown

Join 10,000+ Students

Get our weekly Band 7+ IELTS vocabulary cheat sheet and exam strategies delivered straight to your inbox.